Labor Market

While still in a tight labor market, the number of new hires and workers leaving their current jobs have slowed over the past year. This results in a shrinking share of short-tenure workers. NCCI reports there are 2 to 3 million fewer workers, resulting in a labor shortage. As such, labor supply will likely continue to be a constraint on employment growth. We are presently at full employment as the unemployment rate of 3.4% is below pre-Covid lows. However, this level could rise as Federal Reserve rate hikes slow the economy.

Economy / Inflation

The U.S. economy and labor markets have remained resilient, even with rising interest rates, according to Robert Hartwig, Clinical Associate Professor of Finance at the University of South Carolina, during his presentation at AIS. Mr. Hartwig believes there is a risk of a mild recession later in 2023, and the recent banking failures have increased this risk.

Regarding overall inflation, the U.S. inflation rate (CPI) has already started to ease, after peaking at 9.1% in June 2022. The expectation is that it will be closer to 4% by the latter half of 2023 and closer to 2.5% for 2024. This projected moderation is not linear and is also dependent upon energy prices and Federal Reserve rate hikes.

Medical inflation does not move in lockstep with the CPI. The CPI‑Medical index had risen to 6% during 2022 but was at 1.5% as of March 2023. Since the CPI‑Medical index includes some data that does not pertain to Workers’ Comp, NCCI utilizes an Adjusted CPI‑Medical Index, which is more reflective of Workers’ Comp medical costs. The Adjusted CPI‑Medical index rose to a high of 3.5% in 2022 before heading back down towards 2.5%.

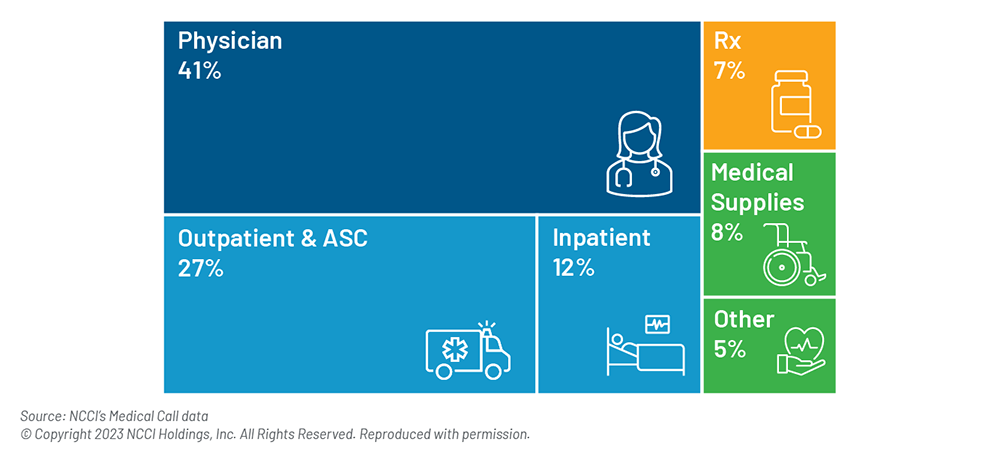

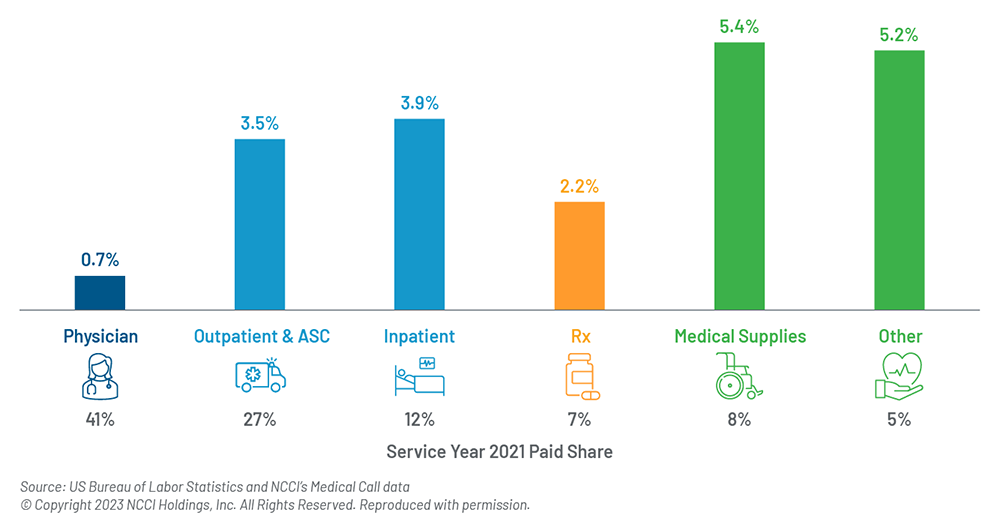

Drilling down further, medical costs that impact Workers’ Comp have both unique price trends and unique utilization trends for each type of medical service. There are many different numbers and data points that go into medical price pressure concerns for Workers’ Comp. As the diagrams below indicate, the physician category, which has the highest distribution in terms of medical spend, is the lowest in terms of price pressure. The categories with the highest price pressure − medical supplies and other (home healthcare, transportation, etc.) − represent a smaller overall share of total medical spend but can be significant on larger claims.

Medical Cost Distribution – Service Year 2021