This is part two of our three-part series – in collaboration with NAMIC – examining inflation and its impact on insurers.

As we moved through 2022, it became increasingly clear the inflationary pressures seen in 2020 and 2021 had settled in for an extended stay. Consumers and businesses scrambled to compensate for skyrocketing costs and inflation levels not seen since the early 1980s. Analysts and commentators warned that the “zero inflation” era seen over the previous decade had come to an end. Now, with some signs suggesting that inflationary pressures have somewhat stabilized, it’s instructive to examine what’s been driving them.

Unanticipated “Shock” Events – COVID and Ukraine

COVID’s 2020 sting left many either unable (due to governmental lockdowns or restrictions) or unwilling (because of varying individual perceptions of risk) to purchase services. Empty planes and “ghost town” central business districts painfully showed the cratering of the service economy. In contrast, consumer demand for goods soared, driven by work-from-home and the desire for personal comfort. Into the mix came the Federal Reserve, cutting its policy rate from 2.25 to zero, and a massive fiscal stimulus package from Congress and the Trump administration. By mid‑2020, real disposable income had expanded on a four-quarter basis at a mid-teens rate while real gross domestic product contracted. Never had this country given itself so much more than it had produced, in turn dislodging a long-term trend of subdued goods prices caused by globalization and technological advances.1

Through 2021 many held the view that as the pandemic subsided, inflation would prove transitory, with Federal Reserve Chair Jerome Powell commenting that “[t]here is little reason to think” that global deflationary forces “have suddenly reversed or abated.”2

Russia’s February 2022 invasion of Ukraine obliterated that prevailing view. Energy supplies were disrupted, and commodity prices nudged upward. Economic sanctions further tangled already-stressed supply chains. The net result? Higher demand for goods with lower, and more costly, supply.3

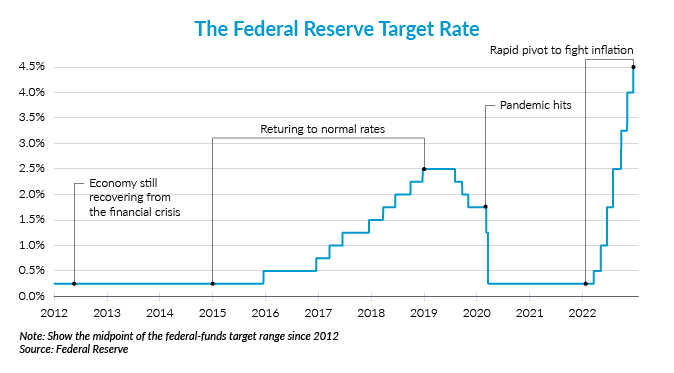

The Federal Reserve

In mid-December, the Federal Reserve approved an interest rate increase of 0.5 percentage point while signaling plans to lift rates in smaller increments through the spring as it works to combat inflation.4 The announcement followed four consecutive larger increases and raised the federal funds rate to a range between 4.25% and 4.5%, a 15‑year high.5 Considered one of the most important interest rates in the U.S. economy, the federal funds rate influences short-term interest rates for everything from home loans to credit cards.6